Notify me when new publications are added.

Qualified North Carolina owners of soundly managed commercial forestland have been eligible for property tax reductions since 1974 through the state’s forestry present-use property tax program. To be eligible for Forestry Present Use Valuation, qualified forestland must be actively engaged in the commercial growing of trees under sound management (NC General Statues 105 277.2- 277.7). Commercial growing of trees will entail a harvest as a thinning, partial, or complete harvest of trees (as prescribed in the forest management plan filed with the county tax office). This publication provides a brief overview of the complicated law.

This publication provides an introduction to the various financial incentives available to woodlot owners. Both federal and state governments offer financial incentive programs; several of these programs provide cost-sharing payments that reimburse landowners for timber management activities. Other programs provide tax incentives, tax credits and deductions for reforestation expenses.

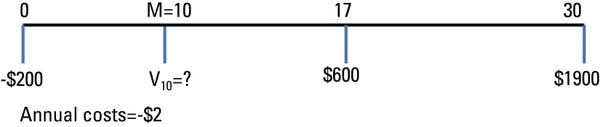

This publication discusses the process for valuing immature timber stands that may have been lost due to natural disasters, theft, or condemnation. It explains the method for valuing young forest stands that may not be appraised under typical timber appraisal methods.